Conspiracy theorists of the world, believers in the hidden hands of the Rothschilds and

the Masons and the Illuminati, we skeptics owe you an apology. You were right. The players may be a little

different, but your basic premise is correct: The world is a rigged game. We found this out in recent months, when

a series of related corruption stories spilled out of the financial sector, suggesting the world's largest banks

may be fixing the prices of, well, just about everything....

It should surprise no one that among the players implicated in this scheme to fix the

prices of interest-rate swaps are the same megabanks – including Barclays, UBS, Bank of America, JPMorgan Chase and

the Royal Bank of Scotland – that serve on the Libor panel that sets global interest rates. In fact, in recent

years many of these banks have already paid multimillion-dollar settlements for anti-competitive manipulation of

one form or another (in addition to Libor, some were caught up in an anti-competitive scheme, detailed in Rolling

Stone last year, to rig municipal-debt service auctions). Though the jumble of financial acronyms sounds like

gibberish to the layperson, the fact that there may now be price-fixing scandals involving both Libor and ISDAfix

suggests a single, giant mushrooming conspiracy of collusion and price-fixing hovering under the ostensibly

competitive veneer of Wall Street culture.

- Rolling Stone -

Everything is rigged the biggest

financial scandal yet

**Please Give Page Time To Load**

The

Markets Are Rigged

The Corbett Report Official LBRY Channel | May 14th, 2021

At base, the markets are a con game where the rich and powerful employ a raft of confidence men

to lure suckers into the latest mania. In this game, the suckers are the general public who are left holding the

bag as the market bubble bursts while the smart money swoops in to buy up the leftover assets at pennies on the

dollar. In this week's edition of The Corbett Report, James Corbett pulls back the curtain on the Wall Street

casino and reveals how the house always wins the rigged games.

The REAL Meaning of GameStop

The Corbett Report Official LBRY Channel | February 7th, 2021

In this conversation (recorded on February 1, 2021) James spells out what the GameStop /

WallStreetBets fiasco was really about. Not that some retail investors were able to squeeze some hedge funds who

were naked short selling and thus "win the game" (spoiler: the government will not allow David to beat Goliath),

but that millions of people have just seen the markets for what they are: A fake and rigged game run by a mafia

that will never allow you to win. This is an educational moment about the power of decentralized movements that

people of all stripes pooh-pooh to their detriment.

If you appreciated this conversation, check out the full hour-long conversation between James

and Pete Quinones on the Freeman Beyond the Wall podcast, which includes a discussion of the historical

technocratic movement and how it evolved into the governing principle of the growing technofascist

dictatorship.

As the major stock indices hit new record highs, many are left wondering how such a bull market can develop

while the average worker faces layoffs, lower wages and rising costs. The answer presents itself in the documented,

admitted and openly acknowledged manipulations of the markets by governments, central bankers, and

institutional banks. This is the GRTV Backgrounder on Global Research TV.

Worship the Stock Market, Wage Slave!

- #PropagandaWatch -

The Corbett Report

First published at 22:04 UTC on August 28th, 2019.

The stock market is an all-seeing, all-knowing, all-powerful diviner's tool. It tells us why the

world is the way it is, where we can expect it to go in the future, and even what people (and entire nations) are

thinking. It is, in fact, God . . . or so the propagandists would have you believe. Find out the real skinny on

the phony baloney stock market in this week's edition of #PropagandaWatch.

In this clip from his regular weekly appearance on Declare Your Independence, James debunks the

"economics" hoax of the language manipulators and defines the "catallactics" solution.

Bestselling author and Mises Institute senior fellow Thomas E Woods, Jr., discusses the

current economic crisis and why government intervention will only make things worse. Recorded at the

University of Colorado, Boulder; 3 April 2009.

THE BUBBLE

Coming in Spring 2013, The Bubble asks the experts who predicted the current recession,

"What happened and why?" Diving deep into the true causes of the financial crisis, renowned economists, investors

and business leaders explain what America is facing if we don't learn from our past mistakes. The film poses the

question: "Is the economy really improving or are we just blowing up another Bubble?"

RON PAUL - THE BUBBLE

The Bubble is a feature length documentary that ask those who predicted the greatest recession since the

Great Depression, why did it happen and what are we facing? The documentary is an adaptation of Tom Woods' New York

Times bestseller Meltdown. Filmmaker Jimmy Morrison is releasing each interview in full for

free before the film's release.

Washington is owned by the private global

banking cartel that owns Wall Street. International law does not apply to this criminal cartel. They stole

trillions of dollars from the American people with help from corrupt politicians over a stretch of many decades,

culminating in the government bailout in 2008, and they have not been held accountable.

These bandits and looters could care less if America crashes and burns. In fact,

they want America to die because they want to institute a private world government upon its ruins. And they’re

doing a fantastic job at it because they’ve had decades of practice in nations in Latin America, Africa, and

Asia where they bought off greedy politicians, and robbed their people through the IMF/World Bank/WTO.

The entire business model of the private global banking tricksters is based on stealing the wealth

of nations, and destroying national independence in order to allow lawless multinational corporations to completely

take over. Read this article about how they do it.

Once nations are put into needless debt by these private global bankers, they put the squeeze on

them by forcing them to pay back usurious loans that make them go bankrupt. After the inevitable mayhem that

follows national collapse, they impose a military dictatorship so that the people can’t resist. Damon Vrabel calls

it the “death of nations.” He writes:

The fact is that most countries are not sovereign (the few that are are being attacked by

CIA/MI6/Mossad or the military). Instead they are administrative districts or customers of the global banking

establishment whose power has grown steadily over time based on the math of the bond market, currently ruled by the

US dollar, and the expansionary nature of fractional lending. Their cult of economists from places like Harvard,

Chicago, and the London School have steadily eroded national sovereignty by forcing debt-based, floating currencies

on countries.

Civilized nations stand up for themselves,

they don’t bow down to private bankers. America can prove to the world that it is civilized, honest, and free by

showing the global banking overlords the door.

The way to fight back against the global robbers at the privately owned Federal Reserve

Bank/IMF/World Bank and the big banks is entirely peaceful. It is a matter of exposing their deviance and deception

to the public, and then hitting the streets. An enemy can’t be defeated unless it remains in the shadows, striking

at will. Directing public light at the private global banking cartel’s evil influence over nations that are thought

to be free and independent by the people is the only way to bring an end to their crimes, and treachery against

Mankind.

A new civilization based on the divine values of freedom, justice, truth, and mutual respect among

nations, and private institutions, can’t be born unless we all come together as global citizens and fight back

against the unlawful rule of the private global banking cartel. Our countries are suffering because of their greed

and ruthless control.

The austerity measures that are being called for by the banks and the elite is bringing chaos onto

the streets of Europe on a scale never before seen, and it won’t be long before America enters the stage. We are

nearing the moment when the globalist conspirators behind the plans for a new world order will openly declare the

end of America. When they do, we shall declare the end of them, and fight for the rebirth of America, and all of

Mankind.

Only an order based on the rule of law and freedom should be accepted. The conspiratorial elite

intend to achieve a new world order through this period of engineered chaos not by law, but by brutal force because

it is the only way to impose a criminal, bank-owned government on a global scale. Despite their rhetoric, these

devilish traitors are not visionary thinkers because corrupt designs for a world state isn’t new in history. Their

arrogance is a cover. They will fail hard. And America will be set free from bondage, along with other nations.

“This is global government, a private corporate global government, taking over every major society

with the same formula. It is fraudulent, and it must be resisted, or we have no future. We cannot allow this new

dark age to begin,” says radio host Alex Jones in a YouTube video message entitled “It’s the Bankers or Us.” Watch

his message, and spread it.

There is a peaceful global revolution against the private global banking cartel, and it can’t be

stopped. Join it and help everyone live free, or die a slave under the empire of debt.

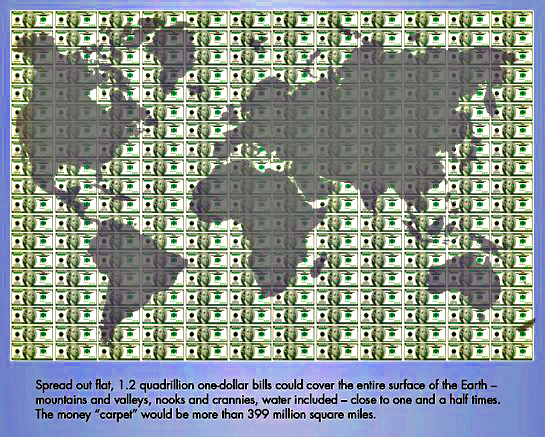

DERIVATIVES: The Debt

Bomb

The derivatives market is the Las Vegas of the world's financial

super elite, worth anywhere between 2 to 8 quadrillion dollars compared to about 70 trillion dollars of world

GDP. We look at the so-called financial innovations of Wall Street from Collateralized Debt Obligations to

Mortgage Backed Securities.

We also look at US government's complicity; White House and Congress both vested

interests not only as recipients of Wall Street largess in the form of campaign donations but as major players with

criminal asymmetrical information and influence advantages.

Everything Is Rigged:

The Biggest Price-Fixing Scandal Ever

The Illuminati were amateurs. The second huge financial

scandal of the year reveals the real international conspiracy: There's

no price the big banks can't fix

GBy Matt Taibbi | April 25, 2013

Conspiracy theorists of the world, believers

in the hidden hands of the Rothschilds and the Masons and the Illuminati, we skeptics owe you an apology. You were

right. The players may be a little different, but your basic premise is correct: The world is a rigged game. We

found this out in recent months, when a series of related corruption stories spilled out of the financial sector,

suggesting the world's largest banks may be fixing the prices of, well, just about everything.

You may have heard of the Libor scandal, in which at least three – and perhaps as many as 16 – of

the name-brand too-big-to-fail banks have been manipulating global interest rates, in the process messing around

with the prices of upward of $500 trillion (that's trillion, with a "t") worth of financial instruments. When that

sprawling con burst into public view last year, it was easily the biggest financial scandal in history – MIT

professor Andrew Lo even said it "dwarfs by orders of magnitude any financial scam in the history of markets."

That was bad enough, but now Libor may have a twin brother. Word has leaked out that the

London-based firm ICAP, the world's largest broker of interest-rate swaps, is being investigated by American

authorities for behavior that sounds eerily reminiscent of the Libor mess. Regulators are looking into whether or

not a small group of brokers at ICAP may have worked with up to 15 of the world's largest banks to manipulate

ISDAfix, a benchmark number used around the world to calculate the prices of interest-rate swaps.

Interest-rate swaps are a tool used by big cities, major corporations and sovereign governments to

manage their debt, and the scale of their use is almost unimaginably massive. It's about a $379 trillion market,

meaning that any manipulation would affect a pile of assets about 100 times the size of the United States federal

budget.

It should surprise no one that among the players implicated in this scheme to fix the prices of

interest-rate swaps are the same megabanks – including Barclays, UBS, Bank of America, JPMorgan Chase and the Royal

Bank of Scotland – that serve on the Libor panel that sets global interest rates. In fact, in recent years many of

these banks have already paid multimillion-dollar settlements for anti-competitive manipulation of one form or

another (in addition to Libor, some were caught up in an anti-competitive scheme, detailed in Rolling Stone last

year, to rig municipal-debt service auctions). Though the jumble of financial acronyms sounds like gibberish to the

layperson, the fact that there may now be price-fixing scandals involving both Libor and ISDAfix suggests a single,

giant mushrooming conspiracy of collusion and price-fixing hovering under the ostensibly competitive veneer of Wall

Street culture.

The Scam Wall Street Learned From the Mafia

Why? Because Libor already affects the prices of interest-rate swaps, making this a

manipulation-on-manipulation situation. If the allegations prove to be right, that will mean that swap customers

have been paying for two different layers of price-fixing corruption. If you can imagine paying 20 bucks for a

crappy PB&J because some evil cabal of agribusiness companies colluded to fix the prices of both peanuts and

peanut butter, you come close to grasping the lunacy of financial markets where both interest rates and

interest-rate swaps are being manipulated at the same time, often by the same banks.

"It's a double conspiracy," says an amazed Michael Greenberger, a former director of the trading

and markets division at the Commodity Futures Trading Commission and now a professor at the University of Maryland.

"It's the height of criminality."

The bad news didn't stop with swaps and interest rates. In March, it also came out that two

regulators – the CFTC here in the U.S. and the Madrid-based International Organization of Securities Commissions –

were spurred by the Libor revelations to investigate the possibility of collusive manipulation of gold and silver

prices. "Given the clubby manipulation efforts we saw in Libor benchmarks, I assume other benchmarks – many other

benchmarks – are legit areas of inquiry," CFTC Commissioner Bart Chilton said.

But the biggest shock came out of a federal courtroom at the end of March – though if you follow

these matters closely, it may not have been so shocking at all – when a landmark class-action civil lawsuit against

the banks for Libor-related offenses was dismissed. In that case, a federal judge accepted the banker-defendants'

incredible argument: If cities and towns and other investors lost money because of Libor manipulation, that was

their own fault for ever thinking the banks were competing in the first place.

"A farce," was one antitrust lawyer's response to the eyebrow-raising dismissal.

"Incredible," says Sylvia Sokol, an attorney for Constantine Cannon, a firm that specializes in

antitrust cases.

All of these stories collectively pointed to the same thing: These banks, which already possess

enormous power just by virtue of their financial holdings – in the United States, the top six banks, many of them

the same names you see on the Libor and ISDAfix panels, own assets equivalent to 60 percent of the nation's GDP –

are beginning to realize the awesome possibilities for increased profit and political might that would come with

colluding instead of competing. Moreover, it's increasingly clear that both the criminal justice system and the

civil courts may be impotent to stop them, even when they do get caught working together to game the system.

If true, that would leave us living in an era of undisguised, real-world conspiracy, in which the

prices of currencies, commodities like gold and silver, even interest rates and the value of money itself, can be

and may already have been dictated from above. And those who are doing it can get away with it. Forget the

Illuminati – this is the real thing, and it's no secret. You can stare right at it, anytime you want.

The banks found a loophole, a basic flaw in the machine. Across the financial system, there are

places where prices or official indices are set based upon unverified data sent in by private banks and financial

companies. In other words, we gave the players with incentives to game the system institutional roles in the

economic infrastructure.

Libor, which measures the prices banks charge one another to borrow money, is a perfect example,

not only of this basic flaw in the price-setting system but of the weakness in the regulatory framework supposedly

policing it. Couple a voluntary reporting scheme with too-big-to-fail status and a revolving-door legal system, and

what you get is unstoppable corruption.

Every morning, 18 of the world's biggest banks submit data to an office in London about how much

they believe they would have to pay to borrow from other banks. The 18 banks together are called the "Libor panel,"

and when all of these data from all 18 panelist banks are collected, the numbers are averaged out. What emerges,

every morning at 11:30 London time, are the daily Libor figures.

Banks submit numbers about borrowing in 10 different currencies across 15 different time periods,

e.g., loans as short as one day and as long as one year. This mountain of bank-submitted data is used every day to

create benchmark rates that affect the prices of everything from credit cards to mortgages to currencies to

commercial loans (both short- and long-term) to swaps.

Gangster Bankers Broke Every Law in the Book

Dating back perhaps as far as the early Nineties, traders and others inside these banks were

sometimes calling up the company geeks responsible for submitting the daily Libor numbers (the "Libor submitters")

and asking them to fudge the numbers. Usually, the gimmick was the trader had made a bet on something – a swap,

currencies, something – and he wanted the Libor submitter to make the numbers look lower (or, occasionally, higher)

to help his bet pay off.

Famously, one Barclays trader monkeyed with Libor submissions in exchange for a bottle of Bollinger

champagne, but in some cases, it was even lamer than that. This is from an exchange between a trader and a Libor

submitter at the Royal Bank of Scotland:

SWISS FRANC TRADER: can u put 6m swiss libor in low pls?...

PRIMARY SUBMITTER: Whats it worth

SWSISS FRANC TRADER: ive got some sushi rolls from yesterday?...

PRIMARY SUBMITTER: ok low 6m, just for u

SWISS FRANC TRADER: wooooooohooooooo.?.?. thatd be awesome

Screwing around with world interest rates that affect billions of people in exchange for day-old

sushi – it's hard to imagine an image that better captures the moral insanity of the modern financial-services

sector.

Hundreds of similar exchanges were uncovered when regulators like Britain's Financial Services

Authority and the U.S. Justice Department started burrowing into the befouled entrails of Libor. The documentary

evidence of anti-competitive manipulation they found was so overwhelming that, to read it, one almost becomes

embarrassed for the banks. "It's just amazing how Libor fixing can make you that much money," chirped one yen

trader. "Pure manipulation going on," wrote another.

Yet despite so many instances of at least attempted manipulation, the banks mostly skated. Barclays

got off with a relatively minor fine in the $450 million range, UBS was stuck with $1.5 billion in penalties, and

RBS was forced to give up $615 million. Apart from a few low-level flunkies overseas, no individual involved in

this scam that impacted nearly everyone in the industrialized world was even threatened with criminal

prosecution.

Two of America's top law-enforcement officials, Attorney General Eric Holder and former Justice

Department Criminal Division chief Lanny Breuer, confessed that it's dangerous to prosecute offending banks because

they are simply too big. Making arrests, they say, might lead to "collateral consequences" in the economy.

The relatively small sums of money extracted in these settlements did not go toward reparations for

the cities, towns and other victims who lost money due to Libor manipulation. Instead, it flowed mindlessly into

government coffers. So it was left to towns and cities like Baltimore (which lost money due to fluctuations in

their municipal investments caused by Libor movements), pensions like the New Britain, Connecticut, Firefighters'

and Police Benefit Fund, and other foundations – and even individuals (billionaire real-estate developer Sheldon

Solow, who filed his own suit in February, claims that his company lost $450 million because of Libor manipulation)

– to sue the banks for damages.

One of the biggest Libor suits was proceeding on schedule when, early in March, an army of

superstar lawyers working on behalf of the banks descended upon federal judge Naomi Buchwald in the Southern

District of New York to argue an extraordinary motion to dismiss. The banks' legal dream team drew from heavyweight

Beltway-connected firms like Boies Schiller (you remember David Boies represented Al Gore), Davis Polk (home of top

ex-regulators like former SEC enforcement chief Linda Thomsen) and Covington & Burling, the onetime

private-practice home of both Holder and Breuer.

The presence of Covington & Burling in the suit – representing, of all companies, Citigroup,

the former employer of current Treasury Secretary Jack Lew – was particularly galling. Right as the Libor case was

being dismissed, the firm had hired none other than Lanny Breuer, the same Lanny Breuer who, just a few months

before, was the assistant attorney general who had balked at criminally prosecuting UBS over Libor because, he

said, "Our goal here is not to destroy a major financial institution."

In any case, this all-star squad of white-shoe lawyers came before Buchwald and made the mother of

all audacious arguments. Robert Wise of Davis Polk, representing Bank of America, told Buchwald that the banks

could not possibly be guilty of anti- competitive collusion because nobody ever said that the creation of Libor was

competitive. "It is essential to our argument that this is not a competitive process," he said. "The banks do not

compete with one another in the submission of Libor."

If you squint incredibly hard and look at the issue through a mirror, maybe while standing on your

head, you can sort of see what Wise is saying. In a very theoretical, technical sense, the actual process by which

banks submit Libor data – 18 geeks sending numbers to the British Bankers' Association offices in London once every

morning – is not competitive per se.

But these numbers are supposed to reflect interbank-loan prices derived in a real, competitive

market. Saying the Libor submission process is not competitive is sort of like pointing out that bank robbers

obeyed the speed limit on the way to the heist. It's the silliest kind of legal sophistry.

But Wise eventually outdid even that argument, essentially saying that while the banks may have

lied to or cheated their customers, they weren't guilty of the particular crime of antitrust collusion. This is

like the old joke about the lawyer who gets up in court and claims his client had to be innocent, because his

client was committing a crime in a different state at the time of the offense.

"The plaintiffs, I believe, are confusing a claim of being perhaps deceived," he said, "with a

claim for harm to competition."

Judge Buchwald swallowed this lunatic argument whole and dismissed most of the case. Libor, she

said, was a "cooperative endeavor" that was "never intended to be competitive." Her decision "does not reflect the

reality of this business, where all of these banks were acting as competitors throughout the process," said the

antitrust lawyer Sokol. Buchwald made this ruling despite the fact that both the U.S. and British governments had

already settled with three banks for billions of dollars for improper manipulation, manipulation that these

companies admitted to in their settlements.

Michael Hausfeld of Hausfeld LLP, one of the lead lawyers for the plaintiffs in this Libor suit,

declined to comment specifically on the dismissal. But he did talk about the significance of the Libor case and

other manipulation cases now in the pipeline.

"It's now evident that there is a ubiquitous culture among the banks to collude and cheat their

customers as many times as they can in as many forms as they can conceive," he said. "And that's not just

surmising. This is just based upon what they've been caught at."

Greenberger says the lack of serious consequences for the Libor scandal has only made other kinds

of manipulation more inevitable. "There's no therapy like sending those who are used to wearing Gucci shoes to

jail," he says. "But when the attorney general says, 'I don't want to indict people,' it's the Wild West. There's

no law."

The problem is, a number of markets feature the same infrastructural weakness that failed in the

Libor mess. In the case of interest-rate swaps and the ISDAfix benchmark, the system is very similar to Libor,

although the investigation into these markets reportedly focuses on some different types of improprieties.

Though interest-rate swaps are not widely understood outside the finance world, the root concept

actually isn't that hard. If you can imagine taking out a variable-rate mortgage and then paying a bank to make

your loan payments fixed, you've got the basic idea of an interest-rate swap.

In practice, it might be a country like Greece or a regional government like Jefferson County,

Alabama, that borrows money at a variable rate of interest, then later goes to a bank to "swap" that loan to a more

predictable fixed rate. In its simplest form, the customer in a swap deal is usually paying a premium for the

safety and security of fixed interest rates, while the firm selling the swap is usually betting that it knows more

about future movements in interest rates than its customers.

Prices for interest-rate swaps are often based on ISDAfix, which, like Libor, is yet another of

these privately calculated benchmarks. ISDAfix's U.S. dollar rates are published every day, at 11:30 a.m. and 3:30

p.m., after a gang of the same usual-suspect megabanks (Bank of America, RBS, Deutsche, JPMorgan Chase, Barclays,

etc.) submits information about bids and offers for swaps.

And here's what we know so far: The CFTC has sent subpoenas to ICAP and to as many as 15 of those

member banks, and plans to interview about a dozen ICAP employees from the company's office in Jersey City, New

Jersey. Moreover, the International Swaps and Derivatives Association, or ISDA, which works together with ICAP (for

U.S. dollar transactions) and Thomson Reuters to compute the ISDAfix benchmark, has hired the consulting firm

Oliver Wyman to review the process by which ISDAfix is calculated. Oliver Wyman is the same company that the

British Bankers' Association hired to review the Libor submission process after that scandal broke last year. The

upshot of all of this is that it looks very much like ISDAfix could be Libor all over again.

"It's obviously reminiscent of the Libor manipulation issue," Darrell Duffie, a finance professor

at Stanford University, told reporters. "People may have been naive that simply reporting these rates was enough to

avoid manipulation."

And just like in Libor, the potential losers in an interest-rate-swap manipulation scandal would be

the same sad-sack collection of cities, towns, companies and other nonbank entities that have no way of knowing if

they're paying the real price for swaps or a price being manipulated by bank insiders for profit. Moreover, ISDAfix

is not only used to calculate prices for interest-rate swaps, it's also used to set values for about $550 billion

worth of bonds tied to commercial real estate, and also affects the payouts on some state-pension annuities.

So although it's not quite as widespread as Libor, ISDAfix is sufficiently power-jammed into the

world financial infrastructure that any manipulation of the rate would be catastrophic – and a huge class of

victims that could include everyone from state pensioners to big cities to wealthy investors in structured notes

would have no idea they were being robbed.

"How is some municipality in Cleveland or wherever going to know if it's getting ripped off?" asks

Michael Masters of Masters Capital Management, a fund manager who has long been an advocate of greater transparency

in the derivatives world. "The answer is, they won't know."

Worse still, the CFTC investigation apparently isn't limited to possible manipulation of swap

prices by monkeying around with ISDAfix. According to reports, the commission is also looking at whether or not

employees at ICAP may have intentionally delayed publication of swap prices, which in theory could give someone

(bankers, cough, cough) a chance to trade ahead of the information.

Swap prices are published when ICAP employees manually enter the data on a computer screen called

"19901." Some 6,000 customers subscribe to a service that allows them to access the data appearing on the 19901

screen.

The key here is that unlike a more transparent, regulated market like the New York Stock Exchange,

where the results of stock trades are computed more or less instantly and everyone in theory can immediately see

the impact of trading on the prices of stocks, in the swap market the whole world is dependent upon a handful of

brokers quickly and honestly entering data about trades by hand into a computer terminal.

Any delay in entering price data would provide the banks involved in the transactions with a rare

opportunity to trade ahead of the information. One way to imagine it would be to picture a racetrack where a giant

curtain is pulled over the track as the horses come down the stretch – and the gallery is only told two minutes

later which horse actually won. Anyone on the right side of the curtain could make a lot of smart bets before the

audience saw the results of the race.

At ICAP, the interest-rate swap desk, and the 19901 screen, were reportedly controlled by a small

group of 20 or so brokers, some of whom were making millions of dollars. These brokers made so much money for

themselves the unit was nicknamed "Treasure Island."

Already, there are some reports that brokers of Treasure Island did create such intentional delays.

Bloomberg interviewed a former broker who claims that he watched ICAP brokers delay the reporting of swap prices.

"That allows dealers to tell the brokers to delay putting trades into the system instead of in real time,"

Bloomberg wrote, noting the former broker had "witnessed such activity firsthand." An ICAP spokesman has no comment

on the story, though the company has released a statement saying that it is "cooperating" with the CFTC's inquiry

and that it "maintains policies that prohibit" the improper behavior alleged in news reports.

The idea that prices in a $379 trillion market could be dependent on a desk of about 20 guys in New

Jersey should tell you a lot about the absurdity of our financial infrastructure. The whole thing, in fact, has a

darkly comic element to it. "It's almost hilarious in the irony," says David Frenk, director of research for Better

Markets, a financial-reform advocacy group, "that they called it ISDAfix."

After scandals involving libor and, perhaps, ISDAfix, the question that should have everyone

freaked out is this: What other markets out there carry the same potential for manipulation? The answer to that

question is far from reassuring, because the potential is almost everywhere. From gold to gas to swaps to interest

rates, prices all over the world are dependent upon little private cabals of cigar-chomping insiders we're forced

to trust.

"In all the over-the-counter markets, you don't really have pricing except by a bunch of guys

getting together," Masters notes glumly.

That includes the markets for gold (where prices are set by five banks in a Libor-ish

teleconferencing process that, ironically, was created in part by N M Rothschild & Sons) and silver (whose

price is set by just three banks), as well as benchmark rates in numerous other commodities – jet fuel, diesel,

electric power, coal, you name it. The problem in each of these markets is the same: We all have to rely upon the

honesty of companies like Barclays (already caught and fined $453 million for rigging Libor) or JPMorgan Chase

(paid a $228 million settlement for rigging municipal-bond auctions) or UBS (fined a collective $1.66 billion for

both muni-bond rigging and Libor manipulation) to faithfully report the real prices of things like interest rates,

swaps, currencies and commodities.

All of these benchmarks based on voluntary reporting are now being looked at by regulators around

the world, and God knows what they'll find. The European Federation of Financial Services Users wrote in an

official EU survey last summer that all of these systems are ripe targets for manipulation. "In general," it wrote,

"those markets which are based on non-attested, voluntary submission of data from agents whose benefits depend on

such benchmarks are especially vulnerable of market abuse and distortion."

Translation: When prices are set by companies that can profit by manipulating them, we're

fucked.

"You name it," says Frenk. "Any of these benchmarks is a possibility for corruption."

The only reason this problem has not received the attention it deserves is because the scale of it

is so enormous that ordinary people simply cannot see it. It's not just stealing by reaching a hand into your

pocket and taking out money, but stealing in which banks can hit a few keystrokes and magically make whatever's in

your pocket worth less. This is corruption at the molecular level of the economy, Space Age stealing – and it's

only just coming into view.

This story is from the May 9th, 2013 issue of Rolling Stone.

From The Archives Issue 1182: May 9, 2013

How HSBC hooked up with drug traffickers and

terrorists.

And got away with it

By Matt Taibbi | February 14, 2013

The deal was announced quietly, just before

the holidays, almost like the government was hoping people were too busy hanging stockings by the fireplace to

notice. Flooring politicians, lawyers and investigators all over the world, the U.S. Justice Department granted a

total walk to executives of the British-based bank HSBC for the largest drug-and-terrorism money-laundering case

ever. Yes, they issued a fine – $1.9 billion, or about five weeks' profit – but they didn't extract so much as one

dollar or one day in jail from any individual, despite a decade of stupefying abuses.

People may have outrage fatigue about Wall Street, and more stories about billionaire greedheads

getting away with more stealing often cease to amaze. But the HSBC case went miles beyond the usual paper-pushing,

keypad-punching sort-of crime, committed by geeks in ties, normally associated with Wall Street. In this case,

the bank literally got away with murder – well, aiding and abetting it, anyway.

Daily Beast: HSBC Report Should Result in Prosecutions, Not Just Fines, Say Critics

For at least half a decade, the storied British colonial banking power helped to wash hundreds of

millions of dollars for drug mobs, including Mexico's Sinaloa drug cartel, suspected in tens of thousands of

murders just in the past 10 years – people so totally evil, jokes former New York Attorney General Eliot Spitzer,

that "they make the guys on Wall Street look good." The bank also moved money for organizations linked to Al Qaeda

and Hezbollah, and for Russian gangsters; helped countries like Iran, the Sudan and North Korea evade sanctions;

and, in between helping murderers and terrorists and rogue states, aided countless common tax cheats in hiding

their cash.

"They violated every goddamn law in the book," says Jack Blum, an attorney and former Senate

investigator who headed a major bribery investigation against Lockheed in the 1970s that led to the passage of the

Foreign Corrupt Practices Act. "They took every imaginable form of illegal and illicit business."

That nobody from the bank went to jail or paid a dollar in individual fines is nothing new in this

era of financial crisis. What is different about this settlement is that the Justice Department, for the first

time, admitted why it decided to go soft on this particular kind of criminal. It was worried that anything more

than a wrist slap for HSBC might undermine the world economy. "Had the U.S. authorities decided to press criminal

charges," said Assistant Attorney General Lanny Breuer at a press conference to announce the settlement, "HSBC

would almost certainly have lost its banking license in the U.S., the future of the institution would have been

under threat and the entire banking system would have been destabilized."

It was the dawn of a new era. In the years just after 9/11, even being breathed on by a suspected

terrorist could land you in extralegal detention for the rest of your life. But now, when you're Too Big to Jail,

you can cop to laundering terrorist cash and violating the Trading With the Enemy Act, and not only will you not be

prosecuted for it, but the government will go out of its way to make sure you won't lose your license. Some on the

Hill put it to me this way: OK, fine, no jail time, but they can't even pull their charter? Are you kidding?

But the Justice Department wasn't finished handing out Christmas goodies. A little over a week

later, Breuer was back in front of the press, giving a cushy deal to another huge international firm, the Swiss

bank UBS, which had just admitted to a key role in perhaps the biggest antitrust/price-fixing case in history, the

so-called LIBOR scandal, a massive interest-raterigging conspiracy involving hundreds of trillions ("trillions,"

with a "t") of dollars in financial products. While two minor players did face charges, Breuer and the Justice

Department worried aloud about global stability as they explained why no criminal charges were being filed against

the parent company.

"Our goal here," Breuer said, "is not to destroy a major financial institution."

A reporter at the UBS presser pointed out to Breuer that UBS had already been busted in 2009 in a

major tax-evasion case, and asked a sensible question. "This is a bank that has broken the law before," the

reporter said. "So why not be tougher?"

"I don't know what tougher means," answered the assistant attorney general.

Also known as the Hong Kong and Shanghai Banking Corporation, HSBC has always been associated with

drugs. Founded in 1865, HSBC became the major commercial bank in colonial China after the conclusion of the Second

Opium War. If you're rusty in your history of Britain's various wars of Imperial Rape, the Second Opium War was the

one where Britain and other European powers basically slaughtered lots of Chinese people until they agreed to

legalize the dope trade (much like they had done in the First Opium War, which ended in 1842).

A century and a half later, it appears not much has changed. With its strong on-the-ground presence

in many of the various ex-colonial territories in Asia and Africa, and its rich history of cross-cultural moral

flexibility, HSBC has a very different international footprint than other Too Big to Fail banks like Wells Fargo or

Bank of America. While the American banking behemoths mainly gorged themselves on the toxic residential-mortgage

trade that caused the 2008 financial bubble, HSBC took a slightly different path, turning itself into the

destination bank for domestic and international scoundrels of every possible persuasion.

Three-time losers doing life in California prisons for street felonies might be surprised to learn

that the no-jail settlement Lanny Breuer worked out for HSBC was already the bank's third strike. In fact, as a

mortifying 334-page report issued by the Senate Permanent Subcommittee on Investigations last summer made plain,

HSBC ignored a truly awesome quantity of official warnings.

In April 2003, with 9/11 still fresh in the minds of American regulators, the Federal Reserve sent

HSBC's American subsidiary a cease-and-desist letter, ordering it to clean up its act and make a better effort to

keep criminals and terrorists from opening accounts at its bank. One of the bank's bigger customers, for instance,

was Saudi Arabia's Al Rajhi bank, which had been linked by the CIA and other government agencies to terrorism.

According to a document cited in a Senate report, one of the bank's founders, Sulaiman bin Abdul Aziz Al Rajhi, was

among 20 early financiers of Al Qaeda, a member of what Osama bin Laden himself apparently called the "Golden

Chain." In 2003, the CIA wrote a confidential report about the bank, describing Al Rajhi as a "conduit for

extremist finance." In the report, details of which leaked to the public by 2007, the agency noted that Sulaiman Al

Rajhi consciously worked to help Islamic "charities" hide their true nature, ordering the bank's board to "explore

financial instruments that would allow the bank's charitable contributions to avoid official Saudi scrutiny." (The

bank has denied any role in financing extremists.)

In January 2005, while under the cloud of its first double-secret-probation agreement with the

U.S., HSBC decided to partially sever ties with Al Rajhi. Note the word "partially": The decision would only apply

to Al Rajhi banking and not to its related trading company, a distinction that tickled executives inside the bank.

In March 2005, Alan Ketley, a compliance officer for HSBC's American subsidiary, HBUS, gleefully told Paul Plesser,

head of his bank's Global Foreign Exchange Department, that it was cool to do business with Al Rajhi Trading.

"Looks like you're fine to continue dealing with Al Rajhi," he wrote. "You'd better be making lots of money!"

But this backdoor arrangement with bin Laden's suspected "Golden Chain" banker wasn't direct enough

– many HSBC executives wanted the whole shebang restored. In a remarkable e-mail sent in May 2005, Christopher Lok,

HSBC's head of global bank notes, asked a colleague if they could maybe go back to fully doing business with Al

Rajhi as soon as one of America's primary banking regulators, the Office of the Comptroller of the Currency, lifted

the 2003 cease-and-desist order: "After the OCC closeout and that chapter is hopefully finished, could we revisit

Al Rajhi again? London compliance has taken a more lenient view."

After being slapped with the order in 2003, HSBC began blowing off its requirements both in letter

and in spirit – and on a mass scale, too. Instead of punishing the bank, though, the government's response was to

send it more angry letters. Typically, those came in the form of so-called "MRA" (Matters Requiring Attention)

letters sent by the OCC. Most of these touched upon the same theme, i.e., HSBC failing to do due diligence on the

shady characters who might be depositing money in its accounts or using its branches to wire money. HSBC racked up

these "You're Still Screwing Up and We Know It" orders by the dozen, and in just one brief stretch between 2005 and

2006, it received 30 different formal warnings.

Nonetheless, in February 2006 the OCC under George Bush suddenly decided to release HSBC from the

2003 cease-and-desist order. In other words, HSBC basically violated its parole 30 times in just more than a year

and got off anyway. The bank was, to use the street term, "off paper" – and free to let the Al Rajhis of the world

come rushing back.

After HSBC fully restored its relationship with the apparently terrorist-friendly Al Rajhi Bank in

Saudi Arabia, it supplied the bank with nearly 1 billion U.S. dollars. When asked by HSBC what it needed all its

American cash for, Al Rajhi explained that people in Saudi Arabia need dollars for all sorts of reasons. "During

summer time," the bank wrote, "we have a high demand from tourists traveling for their vacations."

The Treasury Department keeps a list compiled by the Office of Foreign Assets Control, or OFAC, and

American banks are not supposed to do business with anyone on the OFAC list. But the bank knowingly helped banned

individuals elude the sanctions process. One such individual was the powerful Syrian businessman Rami Makhlouf, a

close confidant of the Assad family. When Makhlouf appeared on the OFAC list in 2008, HSBC responded not by

severing ties with him but by trying to figure out what to do about the accounts the Syrian power broker had in its

Geneva and Cayman Islands branches. "We have determined that accounts held in the Caymans are not in the

jurisdiction of, and are not housed on any systems in, the United States," wrote one compliance officer.

"Therefore, we will not be reporting this match to OFAC."

Translation: We know the guy's on a terrorist list, but his accounts are in a place the Americans

can't search, so screw them.

Remember, this was in 2008 – five years after HSBC had first been caught doing this sort of thing.

And even four years after that, when being grilled by Michigan Sen. Carl Levin in July 2012, an HSBC executive

refused to absolutely say that the bank would inform the government if Makhlouf or another OFAC-listed name popped

up in its system – saying only that it would "do everything we can."

The Senate exchange highlighted an extremely frustrating dynamic government investigators have had

to face with Too Big to Jail megabanks: The same thing that makes them so attractive to shady customers – their

ability to instantaneously move money around the world to places like the Cayman Islands and Switzerland – makes it

easy for them to play dumb with regulators by hiding behind secrecy laws.

When it wasn't banking for shady Third World characters, HSBC was training its mental firepower on

the problem of finding creative ways to allow it to do business with countries under U.S. sanction, particularly

Iran. In one memo from HSBC's Middle East subsidiary, HBME, the bank notes that it could make a lot of money with

Iran, provided it dealt with what it termed "difficulties" – you know, those pesky laws.

"It is anticipated that Iran will become a source of increasing income for the group going

forward," the memo says, "and if we are to achieve this goal we must adopt a positive stance when encountering

difficulties."

The "positive stance" included a technique called "stripping," in which foreign subsidiaries like

HSBC Middle East or HSBC Europe would remove references to Iran in wire transactions to and from the United States,

often putting themselves in place of the actual client name to avoid triggering OFAC alerts. (In other words, the

transaction would have HBME listed on one end, instead of an Iranian client.)

For more than half a decade, a whopping $19 billion in transactions involving Iran went through the

American financial system, with the Iranian connection kept hidden in 75 to 90 percent of those transactions. HSBC

has been headquartered in England for more than two decades – it's Europe's largest bank, in fact – but it has

major subsidiary operations in every corner of the world. What's come out in this investigation is that the chiefs

in the parent company often knew about shady transactions when the regional subsidiary did not. In the case of

banned Iranian transactions, for instance, there are multiple e-mails from HSBC's compliance head, David Bagley, in

which he admits that HSBC's American subsidiary probably has no clue that HSBC Europe has been sending it buttloads

of banned Iranian money.

"I am not sure that HBUS are aware of the fact that HBEU are already providing clearing facilities

for four Iranian banks," he wrote in 2003. The following year, he made the same observation. "I suspect that HBUS

are not aware that [Iranian] payments may be passing through them," he wrote.

What's the upside for a bank like HSBC to do business with banned individuals, crooks and so on?

The answer is simple: "If you have clients who are interested in 'specialty services' – that's the euphemism for

the bad stuff – you can charge 'em whatever you want," says former Senate investigator Blum. "The margin on

laundered money for years has been roughly 20 percent."

Those charges might come in many forms, from upfront fees to promises to keep deposits at the bank

for certain lengths of time. However you structure it, the possibilities for profit are enormous, provided you're

willing to accept money from almost anywhere. HSBC, its roots in the raw battlefield capitalism of the old British

colonies and its strong presence in Asia, Africa and the Middle East, had more access to customers needing

"specialty services" than perhaps any other bank.

And it worked hard to satisfy those customers. In perhaps the pinnacle innovation in the history of

sleazy banking practices, HSBC ran a preposterous offshore operation in Mexico that allowed anyone to walk into any

HSBC Mexico branch and open a U.S.-dollar account (HSBC Mexico accounts had to be in pesos) via a so-called "Cayman

Islands branch" of HSBC Mexico. The evidence suggests customers barely had to submit a real name and address, much

less explain the legitimate origins of their deposits.

If you can imagine a drive-thru heart-transplant clinic or an airline that keeps a fully-stocked

minibar in the cockpit of every airplane, you're in the ballpark of grasping the regulatory absurdity of HSBC

Mexico's "Cayman Islands branch." The whole thing was a pure shell company, run by Mexicans in Mexican bank

branches.

At one point, this figment of the bank's corporate imagination had 50,000 clients, holding a total

of $2.1 billion in assets. In 2002, an internal audit found that 41 percent of reviewed accounts had incomplete

client information. Six years later, an e-mail from a high-ranking HSBC employee noted that 15 percent of customers

didn't even have a file. "How do you locate clients when you have no file?" complained the executive.

It wasn't until it was discovered that these accounts were being used to pay a U.S. company

allegedly supplying aircraft to Mexican drug dealers that HSBC took action, and even then it closed only some of

the "Cayman Islands branch" accounts. As late as 2012, when HSBC executives were being dragged before the U.S.

Senate, the bank still had 20,000 such accounts worth some $670 million – and under oath would only say that the

bank was "in the process" of closing them.

Meanwhile, throughout all of this time, U.S. regulators kept examining HSBC. In an absurdist

pattern that would continue through the 2000s, OCC examiners would conduct annual reviews, find the same disturbing

shit they'd found for years, and then write about the bank's problems as though they were being discovered for the

first time. From the 2006 annual OCC review: "During the year, we identified a number of areas lacking consistent,

vigilant adherence to BSA/AML policies.?.?.?.?Management responded positively and initiated steps to correct

weaknesses and improve conformance with bank policy. We will validate corrective action in the next examination

cycle."

Translation: These guys are assholes, but they admit it, so it's cool and we won't do anything.

A year later, on July 24th, 2007, OCC had this to say: "During the past year, examiners identified

a number of common themes, in that businesses lacked consistent, vigilant adherence to BSA/AML policies. Bank

policies are acceptable.?.?.?.?Management continues to respond positively and initiated steps to improve

conformance with bank policy."

Translation: They're still assholes, but we've alerted them to the problem and everything'll be

cool.

By then, HSBC's lax money-laundering controls had infected virtually the entire company. Russians

identifying themselves as used-car salesmen were at one point depositing $500,000 a day into HSBC, mainly through a

bent traveler's-checks operation in Japan. The company's special banking program for foreign embassies was so

completely fucked that it had suspicious-activity alerts backed up by the thousands. There is also strong evidence

that the bank was allowing clients in Sudan, Cuba, Burma and North Korea to evade sanctions.

When one of the company's compliance chiefs, Carolyn Wind, raised concerns that she didn't have

enough staff to monitor suspicious activities at a board meeting in 2007, she was fired. The sheer balls it took

for the bank to ignore its compliance executives and continue taking money from so many different shady sources

while ostensibly it had regulators swarming all over its every move is incredible. "You can't make up more

egregious money-laundering that permeated an entire institution," says Spitzer.

By the late 2000s, other law enforcement agencies were beginning to catch HSBC's scent. The

Department of Homeland Security started investigating HSBC for laundering drug money, while the attorney general's

office in West Virginia snooped around HSBC's involvement in a Medicare-fraud case. A federal intra-agency meeting

was convened in Washington in September 2009, at which it was determined that HSBC was out of control and needed to

be investigated more closely.

The bank itself was then notified that its usual OCC review was being "expanded." More OCC staff

was assigned to pore through HSBC's books, and, among other things, they found a backlog of 17,000 alerts of

suspicious activity that had not been processed. They also noted that the bank had a similar pileup of subpoenas in

money-laundering cases.

Finally it seemed the government was on the verge of becoming genuinely pissed off. In March 2010,

after seeing countless ultimatums ignored, they issued one more, giving HSBC three months to clear that goddamned

17,000-alert backlog or else there would be serious consequences. HSBC met that deadline, but months later the OCC

again found the bank's money-laundering controls seriously wanting, forcing the government to take,

well?.?.?.?drastic action, right?

Sort of! In October 2010, the OCC took a deep breath, strapped on its big-boy pants

and?.?.?.?issued a second cease-and-desist order!

In other words, it was "Don't Do It Again" – again. The punishment for all of that dastardly

defiance was to bring the regulatory process right back to the same kind of double-secret-probation order they'd

tried in 2003.

Not to say that HSBC didn't make changes after the second Don't Do It Again order. It did – it

hired some people.

In the summer of 2010, 25-year-old Everett Stern was just out of business school, fighting a mild

case of wanderlust and looking for a job but also for adventure. His dream was to be a CIA agent, battling bad guys

and snatching up Middle Eastern terrorists. He applied to the agency's clandestine service, had an interview even,

but just before graduation, the bespectacled, youthfully exuberant Stern was turned down.

He was crushed, but then he found an online job posting that piqued his interest. HSBC, a major

international bank, was looking for people to help with its anti-money-laundering program. "I thought this was

exactly what I wanted to do," he says. "It sounded so exciting."

Stern went up to HSBC's offices in New Castle, Delaware, for an interview, and that October, just

days after the OCC issued the second Don't Do It Again letter, he started work as part of HSBC's "expanded"

antimoney-laundering program.

From the outset, Stern knew there was something weird about his job. "I had to go to the library to

take out books on money-laundering," Stern says now, laughing. "That's how bad it was." There were no training

courses or seminars on money-laundering – what it was, how to detect it. His work mainly consisted of looking up

the names of unsavory characters on the Internet and then running them through the bank's internal systems to see

if they popped up on any account names anywhere.

Even weirder, nobody seemed to care if anybody was doing any actual work. The Delaware office was

mostly empty for a long while, just a giant unpainted room with a few hastily arranged cubicles and only a dozen or

so people in it, and nobody really watching any of the workers. Stern and a fellow co-worker would routinely

finish all their work by 10:30 in the morning, then spend a few hours throwing rocks into a quarry located behind

the bank offices. Then they would go back to their cubicles and hang out until 3 p.m. or so, or until it was at

least plausible that they'd put in a real workday. "If we asked for any more work," Stern says, "they got

angry."

Stern earned a starting salary of $54,900.

Soon enough, though, out of boredom and also maybe a little bit of patriotism, Stern started to

sift through some of the backlogged alerts and tried to make sense of them. Almost immediately, he found a series

of deeply concerning transactions. There was an exchange company wiring large sums of money to untraceable

destinations in the Middle East. A Saudi fruit company was sending millions, Stern found with a simple Internet

search, to a high-ranking figure in the Yemeni wing of the Muslim Brotherhood. Stern even learned that HSBC was

allowing millions of dollars to be moved from the Karaiba chain of supermarkets in Africa to a firm called Tajco,

run by the Tajideen brothers, who had been singled out by the Treasury Department as major financiers of

Hezbollah.

Every time Stern brought one of these discoveries to his bosses, they rolled their eyes at him, if

not worse. When he alerted his boss that a shipping company with ties to Iran was doing a lot of business with the

bank, he blew up. "You called me over for this?" the boss snapped.

Soon after, the empty office started to fill up. What HSBC did in the way of hiring new staff was

actually pretty clever. It liquidated its credit-card-collections unit and moved the bulk of the employees over to

the anti-money-laundering department. Again, without really training anyone at all, it put hundreds of loud,

gum-chewing, mostly uneducated, occasionally rowdy call-center workers on a new gig, turning them into

money-laundering investigators.

Stern says his co-workers not only sucked at their jobs, they didn't even know what their jobs

were. "You could walk into that building today," he says, "and ask anyone there what moneylaundering is – and I

guarantee you, no one will know."

When something fishy pops up in connection with a bank account, the bank generates an alert. An

alert can be birthed by almost anything, from someone wiring $9,999 (to keep under the $10K reporting level) to

someone wiring large sums in round numbers to someone else opening an account with a phony-sounding name or

address.

When an alert gets generated, the bank is supposed to promptly investigate the matter. If the bank

doesn't clear the alert, it creates a "Suspicious Activity Report," which is handed over to the Treasury Department

to be investigated.

Stern then found himself in the middle of a perverse sort-of anticompliance mechanism. HSBC had

"complied" with the government's Don't Do It Again, Again order by hiring hundreds of bodies whom it turned into an

army for whitewashing suspicious transactions. Remember, the complaint against HSBC was not so much that it had

specifically allowed terrorist or drug money through, but that it had allowed suspicious accounts to pile up

without being checked.

The boss at Stern's Delaware office gave his new team goals: Everyone was to try to clear 72 alerts

a week. For those of you keeping score at home, that's nearly two alerts investigated and cleared every hour.

According to Stern, almost any kind of information was good enough to clear an alert. "Basically, if a company had

a website, you could clear them," he says.

Soon enough, HSBC's compliance executives were circulating cheery e-mails. "Great job by some

Delaware professionals in the early part of the week," wrote Stern's boss on June 30th, 2011. The e-mail was

subject-lined, "The 60-plus crowd," signifying accolades to employees who had cleared more than 60 suspicious

transactions that week.

After trying in vain to convince his bosses to at least let him do his job and look for

money-laundering, Stern decided to turn whistle-blower, telling the FBI and other agencies what was going on at the

bank. He left work at HSBC in 2011, fully expecting that the government would drop the hammer on his former

employers.

By that time, numerous agencies, including the Department of Homeland Security, had crawled all the

way up HSBC's backside, among other things examining it as part of a major international narcotics investigation.

In one four-year period between 2006 and 2009, an astonishing $200 trillion in wire transfers (including from

high-risk countries like Mexico) went through without any monitoring at all. The bank also failed to do due

diligence on the purchase of an incredible $9 billion in physical U.S. dollars from Mexico and played a key role in

the so-called Black Market Peso Exchange, which allowed drug cartels in both Mexico and Colombia to convert U.S.

dollars from drug sales into pesos to be used back home. Drug agents discovered that dealers in Mexico were

building special cash boxes to fit the precise dimensions of HSBC teller windows.

Former bailout inspector and federal prosecutor Neil Barofsky, who has helped secure numerous

foreign money-laundering indictments, points out that the people HSBC was doing business with, like Colombia's

Norte del Valle and Mexico's Sinaloa cartels, were "the worst trafficking organizations imaginable" – groups that

don't just commit murder on a mass scale but are known for beheadings, torture videos ("the new thing now," he

says) and other atrocities, none of which happens without money launderers. It's for this reason, Barofsky says,

that drug prosecutors are not shy about dropping heavy prison sentences on launderers. "Frankly, our view of

money-laundering was that it was on par with, and as significant as, the traffickers themselves," he says.

Barofsky was involved in the first extradition of a Colombian national (Pablo Trujillo, a member of

the same cartel that HSBC moved money for) on moneylaundering charges. "That guy got 10 years," says Barofsky.

"HSBC was doing the same thing, only on a much larger scale than my schmuck was doing."

Clearly, HSBC had violated the 2010 Don't Do It Again, Again order. Everett Stern saw it with his

own eyes; so did the OCC and the U.S. Senate, whose Permanent Subcommittee on Investigations decided to target the

company for a yearlong investigation into global money-laundering. The bank itself, in response to the Senate

investigation, acknowledged that it had "sometimes failed to meet the standards that regulators and customers

expect." It would later go on to say that it was even "profoundly sorry."

A few days after Thanksgiving 2012, Stern heard that the Justice Department was about to announce a

settlement. Since he'd left HSBC the year before, he'd had a rough time. Going public with his allegations had

left him emotionally and financially devastated. He'd been unable to find a job, and at one point even applied for

welfare. But now that the feds were finally about to drop the hammer on HSBC, he figured he'd have the satisfaction

of knowing that his sacrifice had been worthwhile.

So he went to New York and sat in a hotel room, waiting for reporters to call for his comments.

When he heard the news that the "punishment" Breuer had announced was a deferred prosecution agreement – a Don't Do

It Again, Again, Again agreement, if you will – he was flabbergasted.

"I thought, 'All that, for nothing?'?" he says. "I couldn't believe it."

The writer Ambrose Bierce once said there's only one thing in the world worse than a clarinet: two

clarinets. In the same vein, there's only one thing worse than a totally corrupt bank: many corrupt banks.

If the HSBC deal showed how much dastardly crap the state could tolerate from one bank, Breuer was

back a week later to show that the government would go just as easy on banks that team up with other banks to

perpetrate even bigger scandals. On December 19th, 2012, he announced that the Justice Department was essentially

letting Swiss banking giant UBS off the hook for its part in what is likely the biggest financial scam of all

time.

The so-called LIBOR scandal, which is at the heart of the UBS settlement, makes Enron look like a

parking violation. Many of the world's biggest banks, including Switzerland's UBS, Britain's Barclays and the Royal

Bank of Scotland, got together and secretly conspired to manipulate the London Interbank Offered Rate, or LIBOR,

which measures the rate at which banks lend to each other. Many, if not most, interest rates are pegged to LIBOR.

The prices of hundreds of trillions of dollars of financial products are tied to LIBOR, everything from commercial

loans to credit cards to mortgages to municipal bonds to swaps and currencies.

If you can imagine executives at Ford, GM, Mitsubishi, BMW and Mercedes getting together every

morning to fix the prices of aluminum and stainless steel, you have a rough idea of what the LIBOR scandal is like,

except that in the car-company analogy, you'd be dealing with absurdly smaller numbers. These are the world's

biggest banks getting together every morning to essentially fix the price of money. Low LIBOR rates are an

indicator that banks are strong and healthy. These banks were faking the results of their daily physicals. In

banking terms, they were juicing.

Two different types of manipulation took place. In 2008, during the heat of the global crash, banks

artificially submitted low rates in order to present an image of financial soundness to the markets. But at other

times over the course of years, individual traders schemed to move rates up or down in order to profit on

individual trades.

There is nobody anywhere growing weed strong enough to help the human mind grasp the enormity of

this crime. It's a conspiracy so massive that the lawyers who are suing the banks are having an extremely difficult

time figuring out how to calculate the damage.

Here's how it works: Every morning, 16 of the world's largest banks submit numbers to a

Londonbased panel indicating what interest rates they're charging other banks to borrow money and what they

themselves are charged. The LIBOR panel then takes those 16 different interest rates, tosses out the four highest

and the four lowest, and averages out the remaining eight to create that day's LIBOR rates – the basis for interest

rates almost everywhere in the world.

The fact that the LIBOR panel tosses out the four highest and lowest numbers every day is an

important detail, because it means that it is difficult to artificially influence the final rate unless multiple

banks are conspiring with each other. One bank lying its ass off and reporting that banks are lending money to each

other basically for free doesn't move the needle much. To really be sure you're creating an artificially low or

high interest rate, you need a bunch of banks on board – and it turns out that they were.

For perhaps as far back as 20 years, banks have been submitting phony numbers, often in concert

with other banks. They did it for a variety of reasons, but the big one, typically, is that a bank trader is

holding some investment tied to LIBOR – bundles of currencies, municipal bonds, mortgages, whatever – that would

earn more money if the interest rate was lower. So what would happen is, some schmuck trader at Bank X would call

the LIBOR submitter and offer him cash, booze, a blow job or just a pat on the back to get him to submit a fake

number that day.

The scandal first blew up last year when the British megabank Barclays admitted to its part in the

fixing of LIBOR rates. British regulators released a cache of disgusting e-mails showing traders from many

different banks cheerfully monkeying around with your credit-card bills, your mortgage rates, your tax bill, your

IRA account, etc., so that they could make out better on some sordid trade they had on that day. In one case, a

trader from an unnamed bank sent an e-mail to a Barclays trader thanking him for helping to fix interest rates and

promising a kickass bottle of bubbly for his efforts:

"Dude. I owe you big time! Come over one day after work, and I'm opening a bottle of

Bollinger."

UBS was the next bank to confess, and its settlement – $1.5 billion in fines – was much the same,

only the e-mails released were, if anything, more disgusting and damning. The British Financial Services Authority

– equivalent to our SEC – discovered thousands of requests to fudge rates over a period of years involving dozens

of different individuals and multiple banks. In many cases, the misdeeds were committed more or less openly, in

writing, with traders and brokers baldly offering bribes in texts and e-mails with an obvious unconcern for

punishment that later, sadly, proved justified.

"I will fucking do one humongous deal with you," begged one UBS trader who wanted a broker to fix

the rate. "I'll pay, you know, $50,000, $100,000."

British regulators aren't hiding the size of the scandal. The UBS settlement demonstrated, without

a doubt, that the LIBOR scandal involved more than just one or two banks, and probably involved hundreds of people

at many of the world's largest and most prestigious financial institutions – in other words, a truly epic case of

anti-competitive collusion that called into question whether the world's biggest banks are innovating a new,

not-entirely capitalist form of high finance. "We have said there are five further institutions under

investigation," says Christopher Hamilton of the FSA. "And there is a large number of individuals as well." (At

press time, another bank, the Royal Bank of Scotland, also settled for LIBOR-related offenses.)

This dovetailed with what Bob Diamond, the former head of Barclays, told the British Parliament the

day after he stepped down last year. "There is an industrywide problem coming out now," he said. Michael Hausfeld,

a famed class-action lawyer who is suing the banks over LIBOR on behalf of cities like Baltimore whose investments

lost money when interest rates were lowered, says the public still hasn't grasped the importance of comments like

Diamond's. "Diamond essentially said, 'This is an industrywide problem,'" Hausfeld says. "But nobody has defined

what this is yet."

Hausfeld's point – that Diamond's "industrywide problem" might be more than just a few guys messing

with rates; it could be a systemic effort to pervert capitalism itself – underscores the extreme miscalculation of

both recent no-prosecution deals.

At HSBC, the bank did more than avert its eyes to a few shady transactions. It repeatedly defied

government orders as it made a conscious, years-long effort to completely stop discriminating between illegitimate

and legitimate money. And when it somehow talked the U.S. government into crafting a settlement over these offenses

with the lunatic aim of preserving the bank's license, it succeeded, finally, in making crime mainstream.

UBS, meanwhile, was a similarly elemental case, in which the offenses didn't just violate the

letter of the law – they threatened the integrity of the competitive system. If you're going to let hundreds of

boozed-up bankers spend every morning sending goofball e-mails to each other, giving each other superhero

nicknames while they rigged the cost of money (spelling-challenged UBS traders dubbed themselves, among other

things, "captain caos," the "three muscateers" and "Superman"), you might as well give up on capitalism entirely

and just declare the 16 biggest banks in the world the International Bureau of Prices.

Thus, in the space of just a few weeks, regulators in Britain and America teamed up to declare

near-total surrender to both crime and monopoly. This was more than a couple of cases of letting rich guys walk.

These were major policy decisions that will reverberate for the next generation.

Even worse than the actual settlements was the explanation Breuer offered for them. "In the world

today of large institutions, where much of the financial world is based on confidence," he said, "a right

resolution is to ensure that counter-parties don't flee an institution, that jobs are not lost, that there's not

some world economic event that's disproportionate to the resolution we want."

In other words, Breuer is saying the banks have us by the balls, that the social cost of putting

their executives in jail might end up being larger than the cost of letting them get away with, well, anything.

This is bullshit, and exactly the opposite of the truth, but it's what our current government

believes. From JonBenet to O.J. to Robert Blake, Americans have long understood that the rich get good lawyers and

get off, while the poor suck eggs and do time. But this is something different. This is the government admitting to

being afraid to prosecute the very powerful – something it never did even in the heydays of Al Capone or Pablo

Escobar, something it didn't do even with Richard Nixon. And when you admit that some people are too important to

prosecute, it's just a few short steps to the obvious corollary – that everybody else is unimportant enough to

jail.

An arrestable class and an unarrestable class. We always suspected it, now it's admitted. So what

do we do?

The Scam Wall Street Learned From the

Mafia

How America's biggest banks took part in a nationwide

bid-rigging conspiracy - until they were caught on tape

By Matt Taibbi | June 21, 2012

Someday, it will go down in history as the

first trial of the modern American mafia. Of course, you won't hear the recent financial corruption case, United

States of America v. Carollo, Goldberg and Grimm, called anything like that. If you heard about it at all, you're

probably either in the municipal bond business or married to an antitrust lawyer. Even then, all you probably heard

was that a threesome of bit players on Wall Street got convicted of obscure antitrust violations in one of the most

inscrutable, jargon-packed legal snoozefests since the government's massive case against Microsoft in the Nineties

– not exactly the thrilling courtroom drama offered by the famed trials of old-school mobsters like Al Capone or

Anthony "Tony Ducks" Corallo.

But this just-completed trial in downtown New York against three faceless financial executives

really was historic. Over 10 years in the making, the case allowed federal prosecutors to make public for the first